Quick answer

Most companies in Bulgaria are currently not directly required to produce full ESG or CSRD reports. However, many are affected indirectly through banks, EU parent companies, investors, or customers. In practice, ESG usually means organising existing data from payroll, invoices, and governance documents to answer requests credibly — not producing sustainability reports, certifications, or marketing narratives.

Why ESG and sustainability are showing up in Bulgarian business life

If you run a company in Bulgaria — local or foreign-owned — ESG and sustainability questions are increasingly coming from:

- banks and leasing companies

- EU-based parent or group companies

- large customers or platforms

- investors, grant bodies, or public tenders

The questions often feel vague, urgent, and poorly explained.

That frustration is justified.

What is happening is not a sudden ideological shift. It is the practical spillover of EU regulation into everyday business relationships.

Large EU companies must report on sustainability.

To report, they need reliable data.

That data increasingly comes from their counterparties — including companies in Bulgaria.

ESG vs CSRD: what’s the difference (without jargon)

ESG: a framework, not a regulation

ESG (Environmental, Social, Governance) is a risk and information framework used by regulators, banks, and investors.

It is:

- not a law

- not a certification

- not a reporting standard on its own

It is simply a way of organising non-financial information about how a company operates.

CSRD: the legal reporting obligation

The Corporate Sustainability Reporting Directive (CSRD) is EU law.

It applies directly to:

- large EU companies

- listed companies (with limited exceptions)

- certain non-EU companies with significant EU activity

Bulgarian law has been amended to transpose CSRD into the Accounting Act. Initial reporting phases apply first to large public-interest entities, with other large companies and any in-scope listed SMEs following later in the decade.

Most Bulgarian companies — especially privately held ones — are not directly in scope.

However, CSRD creates indirect pressure through:

- group reporting requirements

- supplier ESG questionnaires

- financing conditions

- contractual clauses

Who is actually affected in practice

Companies usually not directly in scope

- Privately owned Bulgarian companies below CSRD thresholds

- Service companies with limited headcount and turnover

- Independent operating companies without EU listing

Companies commonly indirectly affected

- Subsidiaries of EU groups

- Manufacturing, IT, outsourcing, logistics, and service suppliers

- Companies applying for bank financing or EU funding

- Businesses operating in regulated or tender-driven sectors

For example, a Bulgarian IT or manufacturing supplier to a large EU group may receive annual ESG questionnaires covering energy use, labour practices, and anti-corruption policies — even though the supplier itself is not a CSRD-reporting entity.

This indirect effect is now the main ESG reality for companies in Bulgaria.

Regulatory Spillover Beyond CSRD

Other EU employment-related initiatives, such as the EU Pay Transparency Directive (Directive (EU) 2023/970), further illustrate how regulatory developments increasingly intersect with ESG themes. While not an ESG regulation itself, the Directive introduces gender pay gap reporting and transparency obligations that affect workforce governance and equality practices.

See our detailed overview: EU Pay Transparency Directive in Bulgaria (2026 Guide)

What ESG really means for most SMEs in Bulgaria (2026)

For small and medium-sized enterprises (SMEs) in Bulgaria, ESG does not mean preparing a sustainability report or adopting complex reporting frameworks.

In practice, ESG for SMEs usually means:

- responding to ESG questionnaires from banks, EU parent companies, or key customers

- explaining existing policies and operational practices

- providing basic, consistent data drawn from accounting, payroll, and internal records

- demonstrating that ESG answers reflect how the business actually operates

Most SMEs are not CSRD-reporting entities, but they are increasingly asked to support someone else’s reporting.

That distinction matters.

For SMEs, ESG is about credibility and proportionality, not completeness. The goal is to provide reliable, defensible answers without creating parallel reporting systems or making commitments that cannot be maintained over time.

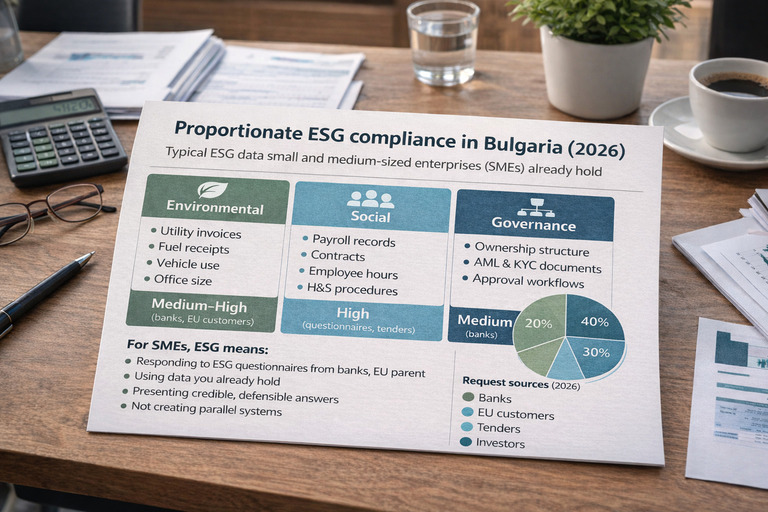

What data companies already have (and often underestimate)

Many ESG requests feel overwhelming because they are presented as something new.

In reality, most companies already hold the majority of required data.

Typical ESG data SMEs already hold

| ESG pillar | Data you likely already have in Bulgaria | Typical request frequency (2026) |

|---|---|---|

| Environmental | Utility invoices, fuel receipts, vehicle use, office size | Medium–High (banks, EU customers) |

| Social | Payroll records, contracts, working hours, H&S procedures | High (questionnaires, tenders) |

| Governance | Ownership structure, AML & KYC files, approval workflows | Medium (banks, investors) |

The governance column in particular — covering ownership structure and AML & KYC documentation — connects directly to Bulgaria’s Anti-Money Laundering framework, which defines what regulated institutions require when verifying corporate structure and beneficial ownership.

What proportionate (“good-enough”) ESG compliance looks like

For most companies in Bulgaria, proportionate ESG compliance means:

- documenting what already exists

- keeping answers consistent year-to-year

- aligning ESG responses with accounting, payroll, and reality

- answering only what is actually being asked

It does not mean:

- publishing ESG reports

- chasing certifications

- making unverifiable sustainability claims

- creating KPIs no one maintains

In ESG, accuracy beats ambition.

Common mistakes companies make

Panic-driven overreaction

Assuming CSRD applies to everyone leads to unnecessary work and cost.

Over-engineering

Complex ESG frameworks that cannot be maintained in practice.

Greenwashing

Vague or exaggerated claims copied from templates or competitors.

Treating ESG as marketing

ESG is increasingly a compliance and risk topic, not a branding exercise.

The critical role of accountants in ESG credibility

Accountants are not sustainability consultants.

But they play a critical role as:

- translators of ESG questions into concrete data

- guardians of consistency

- reality checks between policy and numbers

Good ESG responses must align with:

- payroll records

- energy and cost data

- company structure and governance

This alignment is where professional accounting insight becomes essential for credible, low-risk ESG responses.

Aidos’ position on ESG and sustainability

At Aidos, our stance is simple:

This is not anti-ESG.

It is anti-bullshit.

ESG is compliance work — not ideology, not theatre, not a marketing side-project.

We help companies turn existing records into credible, defensible answers without inventing new systems, chasing certifications, or making promises no one can keep.

Because in ESG, as in accounting, the numbers have to match reality.

For a broader explanation of how this fits into our governance and ethical framework, see our perspective page: 👉 Sustainability & ESG — A Practical Perspective

The wider ESG landscape (briefly)

Other EU initiatives, such as the Corporate Sustainability Due Diligence Directive (CSDDD), further reinforce supply-chain pressure. These rules primarily target large groups, but their effects reach smaller companies indirectly through data requests, contractual clauses, and risk assessments.

For most Bulgarian companies, the impact remains indirect — but real.

Conclusion

ESG and sustainability in Bulgaria are not about perfection.

They are about:

- proportionality

- consistency

- honesty

For most companies, ESG is manageable when treated as a structured extension of existing compliance, not as a parallel reporting ideology.

That is where “good-enough” becomes not only acceptable — but correct.

If your company is receiving ESG questions from banks, parent companies, or customers and you want to respond accurately, proportionately, and without over-engineering, you can contact Aidos to discuss how this fits into your existing accounting and compliance setup.

FAQ – ESG & sustainability for companies in Bulgaria

Do companies in Bulgaria need to comply with CSRD?

Most do not directly at present. Many are indirectly affected through banks, customers, or group reporting.

Do SMEs in Bulgaria need to comply with CSRD?

In most cases, no. The majority of SMEs are currently not directly in scope, but they are often indirectly affected via ESG data requests.

How should SMEs respond to ESG questionnaires?

SMEs should base ESG responses on existing data from payroll, utility invoices, internal policies, and governance documents. Answers should be accurate, consistent, and proportionate.

Does my small Bulgarian company need to hire an ESG consultant?

Usually not. Unless a specific bank, investor, or contract explicitly requires it, most SME ESG needs can be handled using existing data with accounting support.

What happens if I give incomplete ESG answers?

Depending on who is asking, this can lead to delayed financing, follow-up requests, or contractual issues. Consistency and honesty reduce most risks.

Where should a Bulgarian company start with ESG?

Start by reviewing payroll, utility invoices, and corporate governance documents against common ESG questionnaire topics. Build answers from what you already do, and avoid new commitments you cannot maintain.

Disclaimer

This article is for general informational purposes only and does not constitute accounting, tax, legal, or sustainability advice. Requirements depend on company size, sector, and group structure. Professional advice should be obtained for specific cases.

Last reviewed and updated: March 2026

© 2011–2026 Aidos Accountancy Services. All rights reserved.