Quick Answer

A foreign company that wants to employ a person working remotely from Bulgaria does not need to establish a Bulgarian entity. Instead, it can register directly with the Bulgarian National Revenue Agency (NRA) as a foreign employer and insurer. Once registered, the company runs standard monthly payroll and social security declarations for the employee under Bulgarian law. The process is straightforward, but a few structural and tax considerations — particularly around permanent establishment — are worth understanding before the first contract is signed.

Who This Applies To

Companies operating across borders increasingly hire talent in countries where they have no legal presence. Bulgaria is no exception: as a cost-competitive EU member state with a flat 10% income tax and comparatively low social security contributions, it attracts remote workers employed by UK, German, Dutch, and other foreign companies.

Bulgarian law accommodates this through a specific registration path. Foreign employer registration with the NRA in Bulgaria allows a company that employs a Bulgarian-resident worker — or a foreign national working remotely from Bulgaria — to satisfy its payroll and social insurance obligations here without establishing a local entity. This does not require incorporation in the Commercial Register, and it does not create a Bulgarian entity. It simply establishes the employer’s obligation to withhold and remit payroll taxes and social security contributions on behalf of the employee.

This route is commonly used by EU companies hiring one or several remote workers, by UK companies employing staff in Bulgaria since Brexit, and by US, Middle Eastern, or other non-EU businesses with a Bulgarian remote team member.

The Registration Process

What the NRA Registration Covers

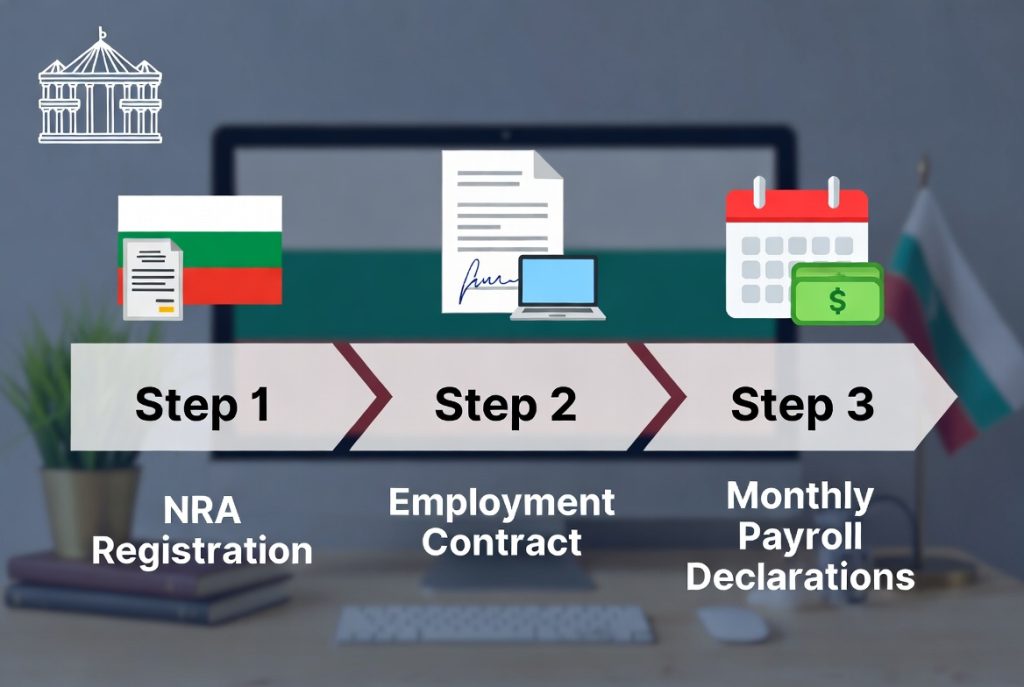

The foreign employer registration with the NRA is a payroll and social security registration — not a commercial or tax registration in the corporate sense. Its purpose is to give the foreign company an insurer identification number, which it then uses to file monthly social security declarations and remit contributions and income tax on behalf of its Bulgarian-based employee.

Registration is initiated by the employer, typically through a licensed representative in Bulgaria acting under a power of attorney. The representative submits the application, manages the registration process, and handles ongoing compliance once the number is issued.

Documents and Information Required

The exact documentation may vary slightly depending on the company’s country of incorporation, but the following is generally required:

- Company details: legal name, registered address, country of incorporation, registration or VAT number, and the details of an authorised representative

- Power of attorney authorising a Bulgarian-based service provider to represent the company before the NRA

- The employee’s personal data, Bulgarian address, and national identification number; foreign nationals working in Bulgaria may need an NRA-issued foreign identification number, which can also be obtained via the same representative

The NRA issues the employer registration number once the application is processed. Timelines vary but one to two weeks is a reasonable expectation under standard conditions.

Monthly Payroll Obligations

Once registered, the foreign employer’s monthly obligations mirror those of any Bulgarian company employing staff. The core framework is set out in the Bulgarian Social Insurance Code and the Personal Income Tax Act. In practical terms, this means:

- Calculating gross-to-net salary each month, including employer and employee social security and health insurance contributions

- Preparing and submitting Declaration Form 1 (individual social insurance data for the employee) and Declaration Form 6 (aggregated contributions and advance income tax)

- Remitting social security contributions and the 10% advance income tax to NRA bank accounts by the 25th of the following calendar month

- Issuing the employee’s annual income certificate under Article 45, paragraph 1 of the Personal Income Tax Act by the end of February for the preceding year

A detailed breakdown of contribution rates, thresholds, and the overall employer cost structure is covered in our Payroll in Bulgaria guide.

Social Security Coordination: EU vs. Non-EU Employers

For EU-based employers, social security coordination is governed by Regulation (EC) No 883/2004 on the coordination of social security systems. The applicable legislation depends on the employee’s working pattern, the employer’s location, and whether any A1 determination or cross-border telework arrangement applies. In many straightforward cases — where an employee resides and works exclusively in Bulgaria for a foreign employer — Bulgarian social security will apply. However, this is not automatic, and the position should be confirmed before employment begins. It is also worth noting that Bulgaria has not signed the EU Framework Agreement on cross-border telework, which means the extended home-working thresholds available under that agreement do not apply here; the standard Regulation 883/2004 rules govern instead.

Where the working arrangement is anything other than exclusive single-country remote work — for example, where the employee splits time between Bulgaria and another country, or where a posting situation may apply — a formal determination of the applicable legislation and potentially an A1 certificate should be obtained before employment begins.

Non-EU employers, including UK companies following Brexit, fall outside Regulation 883/2004. The applicable social security rules depend on whether a bilateral social security agreement exists between Bulgaria and the employer’s country of incorporation. Where no such agreement applies, Bulgarian social security contributions are generally due in Bulgaria for a person residing and working there. This should be verified on a case-by-case basis.

Permanent Establishment: A Consideration, Not a Barrier

One question that arises regularly in this context is whether hiring a remote worker in Bulgaria could create a permanent establishment (PE) for the foreign company — and with it, corporate tax obligations in Bulgaria.

For a single remote worker carrying out their own tasks from a home office, with no authority to conclude contracts on the employer’s behalf, no local revenue-generating activity, and no fixed place of business in Bulgaria, the PE risk is often lower than employers expect under both Bulgarian domestic law and OECD guidelines. Bulgarian corporate tax exposure typically arises where a company has a fixed place of business, a dependent agent who habitually concludes contracts, or a branch.

That said, permanent establishment is a fact-specific analysis. If the employee’s role involves client-facing activity in Bulgaria, contract negotiation on the employer’s behalf, or there are plans to open a branch office or local entity at a later stage, the PE question deserves a separate assessment. Our tax advisory team can assist with that review.

What the Foreign Employer Does Not Need

It is worth being explicit about what the foreign employer registration does not entail, since this is often a source of confusion:

- No Bulgarian company or branch is required solely to employ a remote worker

- No Bulgarian corporate tax return is required where there is no permanent establishment

- No Bulgarian VAT registration arises solely from this employment relationship

- No annual financial statements are filed in Bulgaria where there is no Bulgarian entity

The scope of obligation is limited to payroll, social security, and employment income tax. For companies considering a more substantive Bulgarian presence — whether through a local entity or branch — the Bulgaria Business & Tax Knowledge Hub provides a structured overview of the relevant considerations.

Bulgarian legislation does allow certain social security obligations to be transferred to the employee by agreement, rather than handled by the employer directly. In practice, however, most foreign employers opt to register with the NRA themselves. Direct employer registration provides greater compliance certainty, aligns with standard Bulgarian employer obligations, and reduces the administrative and legal exposure that can arise when social security responsibility rests with the individual employee.

When a Bulgarian Entity May Be Preferable

Foreign employer registration is well suited to companies hiring one or a small number of remote workers with no broader operational footprint in Bulgaria. There are situations, however, where establishing a Bulgarian entity — whether a company or a branch — is the more appropriate structure:

- The business intends to hire a larger local team or expand operations significantly in Bulgaria

- The company will contract directly with Bulgarian customers or generate local revenue

- There is a need for local management, a physical premises, or ongoing commercial activity in Bulgaria

- The employee’s role creates a substantive PE risk that would be better addressed through a formal local structure

Conclusion

Foreign employer registration with the Bulgarian NRA is a well-established and practical mechanism that allows EU and non-EU companies to employ Bulgarian-based remote workers without establishing a local entity. The registration itself is straightforward; the ongoing obligations are predictable; and the costs — both administrative and in terms of employer contributions — are competitive by European standards.

The main area requiring careful attention is social security coordination for EU employers, and the permanent establishment question for companies whose operations may extend beyond a single remote worker. Both are manageable with proper advice at the outset.

Where an engagement involves multiple jurisdictions — payroll obligations in Bulgaria, employment law questions in the employer’s home country, or social security coordination across borders — Aidos operates as part of the Aliant+ international advisory network. That means Aidos can coordinate with member firms and trusted advisers in the relevant countries where payroll, employment law, corporate tax, or social security questions arise simultaneously across borders — removing the complexity of managing multiple unconnected advisors.

How Aidos Can Help

If your company is considering hiring a remote employee in Bulgaria, Aidos can manage the full registration and ongoing payroll compliance process. You may explore our accounting and payroll services or contact us to book a meeting for a tailored assessment of your situation.

Frequently Asked Questions

Does a foreign company need to set up a Bulgarian company to hire one remote employee?

No. A foreign company can register directly with the Bulgarian National Revenue Agency as a foreign employer and insurer. This allows it to run payroll and remit social security contributions for a Bulgarian-based employee without incorporating a Bulgarian entity or branch. A local representative acting under a power of attorney typically handles the registration.

How long does NRA foreign employer registration take?

Under standard conditions, the process takes approximately one to two weeks from the submission of a complete application. Timelines may vary depending on NRA processing volumes and how quickly the employer provides the required documents, including the power of attorney and employee personal data.

What are the main monthly obligations after registration?

The registered foreign employer must calculate payroll monthly, submit Declaration Form 1 and Declaration Form 6 to the NRA, and remit social security contributions and advance income tax by the 25th of the following month. An annual income certificate must also be issued to the employee by the end of February for the preceding calendar year.

Does hiring a remote worker in Bulgaria create corporate tax exposure?

Not automatically. A single remote worker based at home, without authority to conclude contracts or generate local revenue on the employer’s behalf, does not typically create a permanent establishment under Bulgarian law or OECD guidelines. However, permanent establishment is a fact-specific analysis and should be assessed individually where the employee’s role is more complex.

Do different rules apply for UK companies compared to EU companies?

Yes, in terms of social security coordination. For EU employers, the applicable social security legislation depends on the employee’s working pattern and applicable Regulation 883/2004 rules; Bulgarian contributions often apply where the employee resides and works exclusively in Bulgaria, but this should be confirmed before employment begins. Bulgaria has not signed the EU Framework Agreement on cross-border telework, so standard coordination rules apply. UK companies post-Brexit fall outside Regulation 883/2004 entirely; the position depends on any bilateral social security agreement and should be assessed individually.

Disclaimer

This article is for informational purposes only and does not constitute tax, legal, or accounting advice. Each case requires individual assessment under Bulgarian and applicable international law.

Last reviewed: June 2026

© 2011–2026 Aidos Accountancy Services. All rights reserved.