Company cars offer both practicality and prestige — but in Bulgaria, they also come with important tax, VAT, and accounting considerations. Whether you’re purchasing or leasing a vehicle, reimbursing fuel, or managing private vs. business use, staying compliant with the National Revenue Agency (NRA) can help avoid penalties and optimize your tax position.

In this guide, we’ll cover:

- ✅ Tax treatment of company cars

- ✅ VAT rules for purchasing, leasing, and fuel

- ✅ Deductible costs & depreciation

- ✅ Logbook requirements

- ✅ Practical tips for Bulgarian businesses

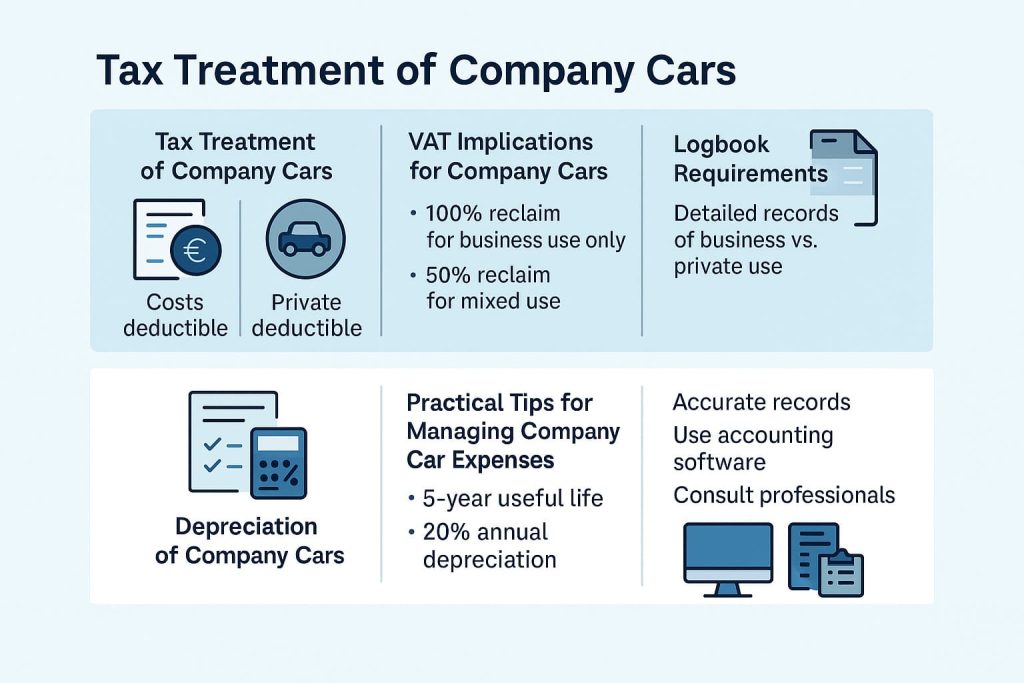

1. Tax Treatment of Company Cars in Bulgaria

In Bulgaria, company cars are treated as business assets. If used strictly for business, related expenses are fully deductible. However, if a vehicle is used for mixed business and personal purposes, deductions must be adjusted.

🧾 Deductible Costs Include:

- Fuel costs (business use only)

- Maintenance & repairs

- Insurance premiums

- Leasing payments

- Depreciation of the asset (see Section 4)

🚫 Private Use Restrictions:

Only business-use expenses are deductible. Keep a logbook to track business vs. private mileage.

🚗 Minimum Seat Requirement:

There’s no official seat requirement. However, the vehicle must be justifiable for business needs (e.g., transporting clients).

Quick Summary: Tax Rules for Company Cars in Bulgaria

2. VAT Implications

Under Bulgarian tax law, passenger cars (up to 6+1 seats) generally cannot reclaim VAT on purchase, fuel, or repairs—unless used for specific commercial activities like taxi services, driving schools, or emergency medical care (see exceptions below). However, operating costs (fuel, repairs, insurance) are still deductible for corporate income tax (CIT) if the car is used for business purposes.

When Can You Reclaim VAT?

✅ For vehicles with 6+1+ seats and registered as category N1 (e.g., cargo vans, SUVs for commercial use):

- 100% VAT reclaim if used exclusively for business.

- 50% VAT reclaim for mixed use.

✅ For passenger cars (up to 6+1 seats), VAT is only reclaimable if used for:

- Taxi services

- Driver training (driving schools)

- Rental/leasing businesses

- Security transport

- Courier/postal services (Note: Delivery of samples/goods by non-courier staff doesn’t qualify)

- Emergency medical vehicles

Corporate Tax Deductions (CIT)

- All company cars (including passenger vehicles) can deduct operating costs (fuel, repairs, insurance) if used for business purposes.

- Required proof: Logbook + roadworthiness certificates.

- Accepted business uses: Client visits, sales reps, management travel, business trips, sample deliveries (non-courier).

3. Logbook Requirements 📒

Maintaining a logbook is mandatory if a vehicle has any private use.

Logbook Should Include:

- Date & purpose of each trip

- Distance driven

- Fuel usage

- Calculated percentage of business use

A well-maintained logbook:

- ✔️ Supports accurate deductions

- ✔️ Ensures VAT compliance

- ✔️ Serves as audit-proof evidence

4. Depreciation of Company Cars

Depreciation allows you to recover the cost of the vehicle over time.

Depreciation Rules:

- Useful life: 5 years

- Rate: 20% annually (on net value)

- Residual value: 10% of initial cost

💰 Example:

Car purchased for BGN 50,000 (excl. VAT):

- Annual depreciation = BGN 10,000

- After 5 years = BGN 50,000 total depreciation

- Residual value = BGN 5,000

5. Practical Tips for Managing Company Car Expenses

🔍 Optimize your tax strategy with these best practices:

- Keep personal and business use separate

- Maintain complete records and logs

- Use accounting software for tracking

- Consult a professional accountant (like Aidos)

Related Articles

- 🔗 Car Registration Bulgaria: Step-by-Step Guide

- 🔗 Tax Deductible Expenses in Bulgaria: A Complete Guide

- 🔗 Maximising Tax Benefits: Managing Business Trips in Bulgaria

How Aidos Accountants Can Help

We offer full support for businesses managing company car-related costs, including:

- ✔️ Expense tracking & logbook templates

- ✔️ Accurate VAT recovery & deduction strategies

- ✔️ Depreciation planning

- ✔️ Audit-ready financial reports

- ✔️ Ongoing consulting for legal compliance

📞 Contact Us

Need help with Company Cars in Bulgaria?

👉 Prefer email? Fill out the contact form below:

❓ Frequently Asked Questions (FAQ)

- Are company car expenses tax-deductible in Bulgaria?

Yes, expenses such as fuel, insurance, repairs, leasing, and depreciation are tax-deductible if the vehicle is used for business purposes. If the car is used for both business and private purposes, only the business-related portion is deductible. - Can I deduct 100% of the VAT on a company car in Bulgaria?

Only if the vehicle is used exclusively for business. For mixed use (business and private), only 50% of the VAT is deductible. (For vehicles with 6+1+ seats and registered as category N1 (e.g., cargo vans, SUVs for commercial use)) - What is required to prove business use of a company car?

A detailed logbook must be maintained, recording trip dates, purposes, kilometers driven, and fuel consumption. This log is essential for both tax compliance and VAT claims. - What is the depreciation rate for company cars in Bulgaria?

The standard rate is 20% annually over 5 years, based on the vehicle’s purchase price (excluding VAT). A residual value of 10% is typically assumed at the end of this period. - Are there restrictions on the type of car that qualifies as a company vehicle?

There’s no strict seat or vehicle type requirement, but the car must be reasonable and justifiable for business use. - Can private use of a company car affect tax deductions?

Yes. Private use reduces the proportion of expenses and VAT that can be claimed as a business deduction. Accurate tracking is essential. - Do I need a separate car for personal and business use?

It’s not required, but having separate vehicles makes recordkeeping and compliance simpler and often maximizes tax benefits. - What happens if I don’t keep a logbook?

Without a logbook, tax authorities may deny deductions and VAT claims, or assume mixed use, reducing eligible amounts. - Can I deduct fuel costs for a passenger car (5 seats) used for sales visits?

Yes, for CIT—but no VAT reclaim unless it meets exception criteria (e.g., taxi services).

Disclaimer

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Consult a qualified accountant or legal professional for advice specific to your situation.